Last year closed with a Phase One agreement to “reset the relationship” between the U.S. and China. Roughly the same time, the first cases of the novel coronavirus were presenting themselves in Wuhan. The COVID-19 pandemic’s impact on global markets will dwarf the effects of any trade policy shifts… and likely leave them changed forever.

Big changes in long-established trade patterns were already underway in 2019. To start with, the weight of U.S. trade policies – including the liberal imposition of tariffs – pushed imports down, while the shale revolution lifted crude oil exports. As a result, the U.S. goods and service trade deficit declined 1.7% to $616.8 billion last year – the first annual decrease since 2013.

The U.S. trade deficit with China declined $64.9 billion from $419.5 billion in 2018 to $345.6 billion in 2019.

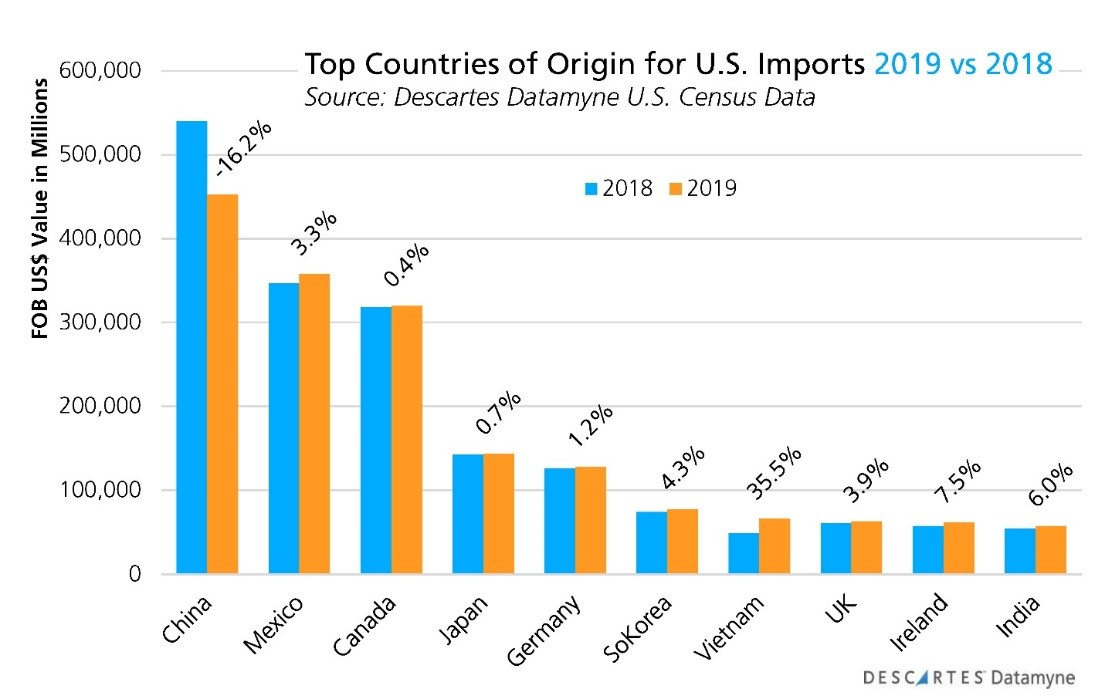

The Descartes Datamyne U.S. Census data on trade in goods indicates a decline in value of 1.74% for imports in 2019. [All values are free on board – FOB – US$ values.] The data makes clear the extent to which the back-and-forth tariff updates since 2018 have throttled the flow of goods between the U.S. and China, with U.S. imports from China falling 16.2%, and U.S. exports to China losing 11.4% in value last year:

Vietnam saw a big gain of 35.5% in the value of imports shipped to the U.S. in 2019 compared with the preceding year. Vietnam also vaulted to No. 7 in 2019, up from the previous year’s ranking as No. 12 among U.S. sources for imports.

Benefiting from the trade dispute between the United States and China , Vietnam is poised to join the select company of entrepôt nations whose exports exceed their domestic production, as the Financial Times reports. The others are Luxembourg, Singapore, Hong Kong, Malta, and Ireland. Vietnam’s arrival as a super-exporter may be delayed by COVID-19, but appears to be inevitable.

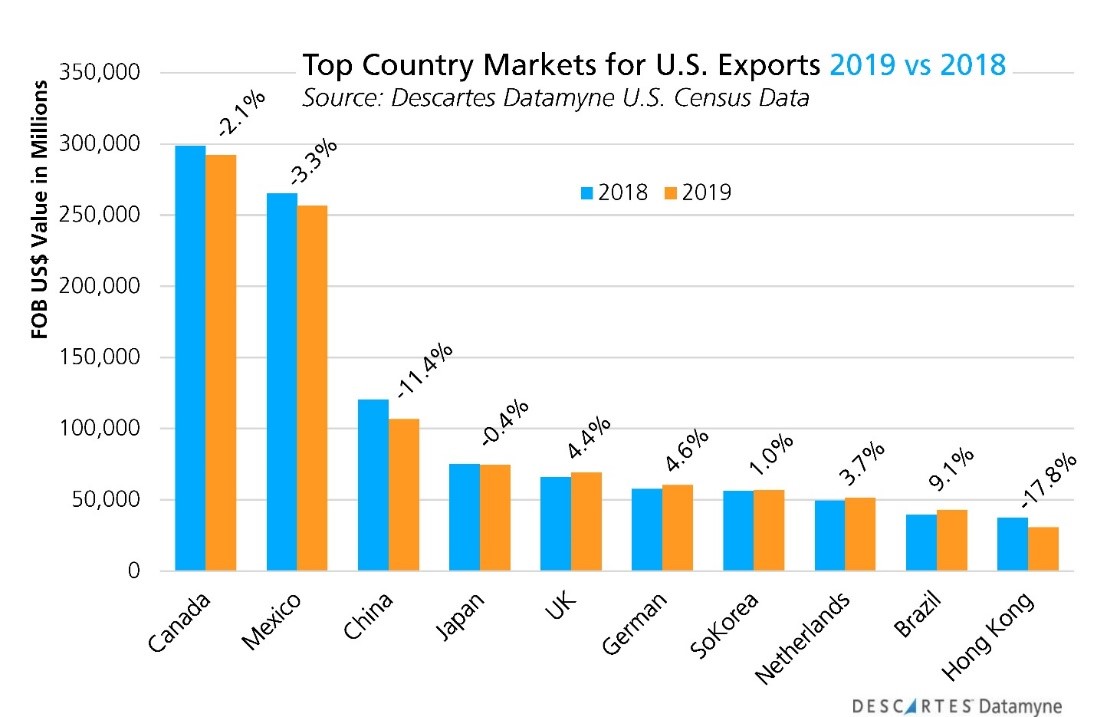

Our Census data also records a 1.13% decline in U.S. exports last year. Losses were steepest in goods bound for China (down 11.4%) and Hong Kong (off 17.8%), but U.S. exports to North American neighbors Canada and Mexico also faltered, as the graph summarizes:

Note that the gains in exports to South Korea and the Netherlands were fueled by crude oil, with South Korea increasing its purchases by $3.5 billion and the Netherlands by $3.0 billion.

COVID-19: Changing Trade Relationships

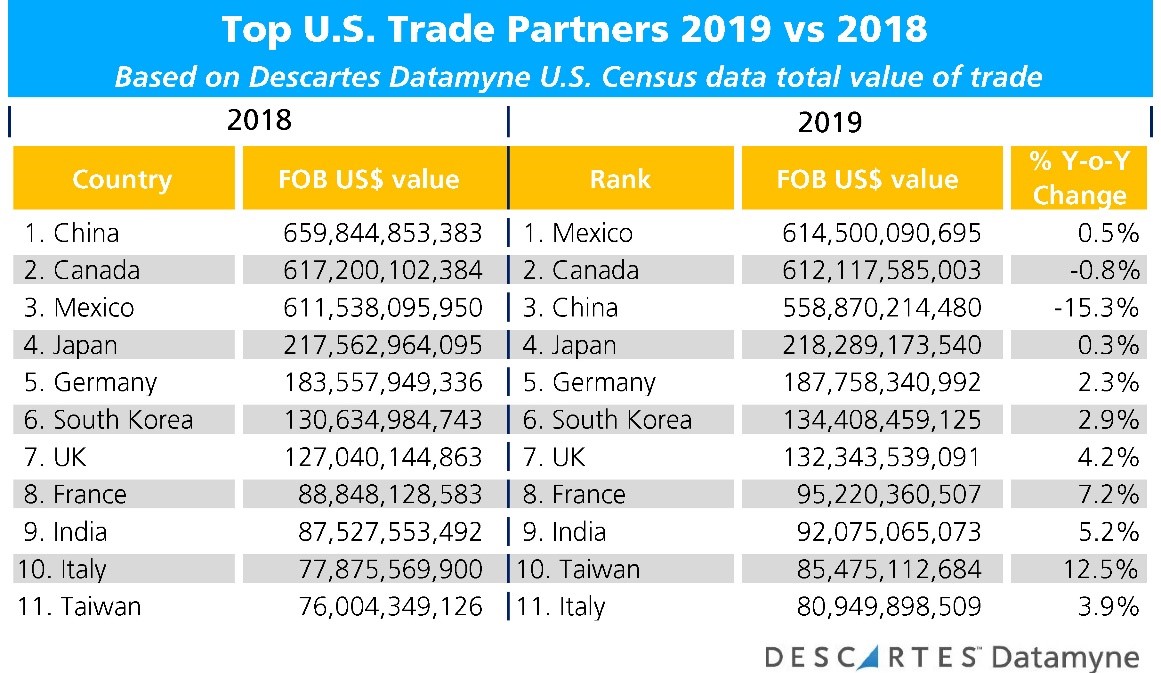

One of the big changes in U.S. trade relations over the past has been the ascendancy of Mexico to the top ranking among U.S. trade partners, based on the combined value of trade in both directions. Canada is No. 2. Erstwhile leader China has slipped to No. 3, as this data table shows:

While shifting trade policy has diminished China’s standing among U.S. trade partners, Mexico’s rise is not solely the result of China’s decline. As we reported last May, Mexico has been growing its exports and moved up the ranks of the world’s exporters from No. 15 to No. 12 in the five years from 2014 through 2018 (the last calendar year for which global data is available.).

The U.S.-Mexico-Canada Agreement (USMCA), that replaces the North American Free Trade Agreement, retools – and very likely will strengthen – this trade bloc’s relations for the upcoming decade.

Last to ratify USMCA, Canada’s Parliament voted to adopt the pact March 13 – just ahead of adjourning for three weeks in an effort to help stop the spread of COVID-19, as Reuters reports. The U.S. announced on March 18 that it would close its border with Canada to “non-essential traffic,” but trade would continue unimpeded.

Meanwhile, COVID-19 might compromise China’s ability to boost its purchases of U.S. products, a cornerstone of the Phase 1 agreement, by $200 billion over the benchmark year of 2017.

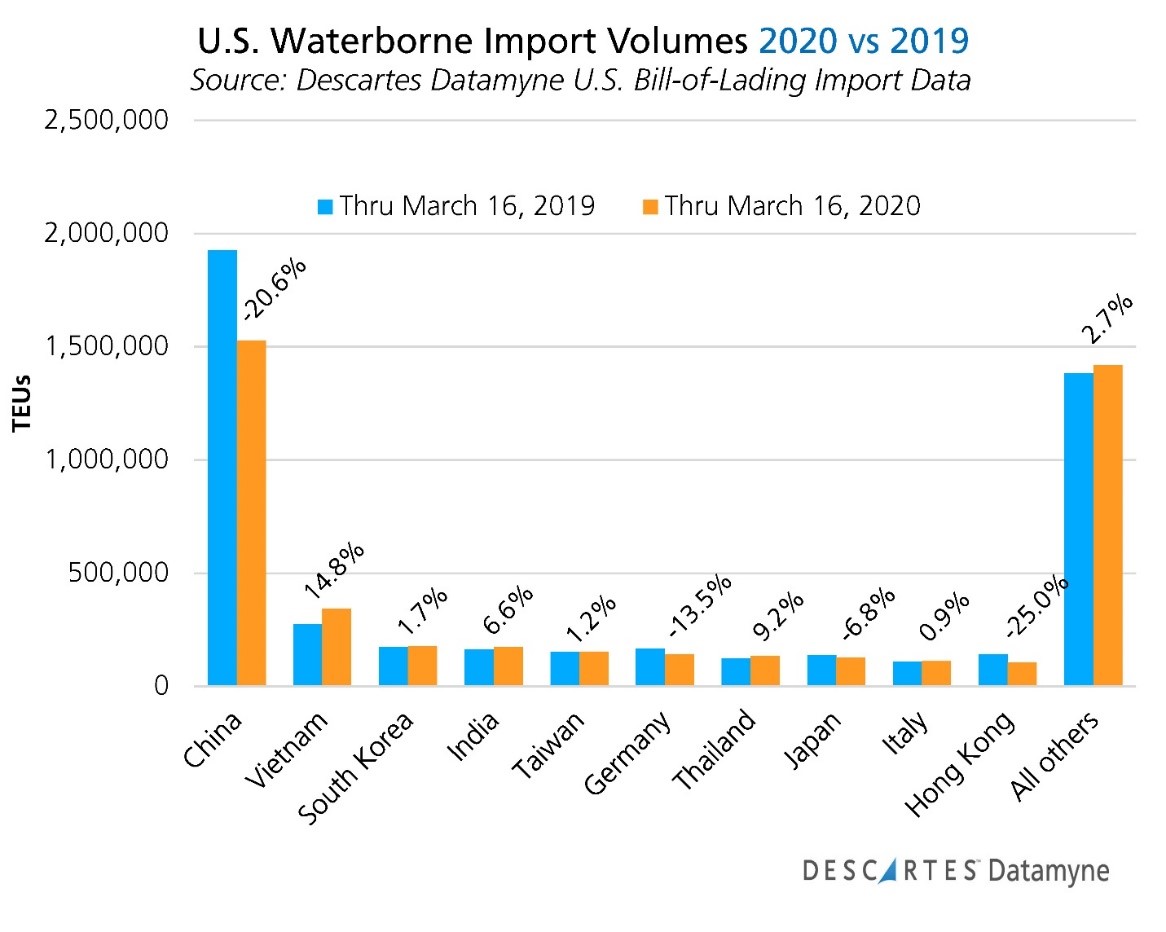

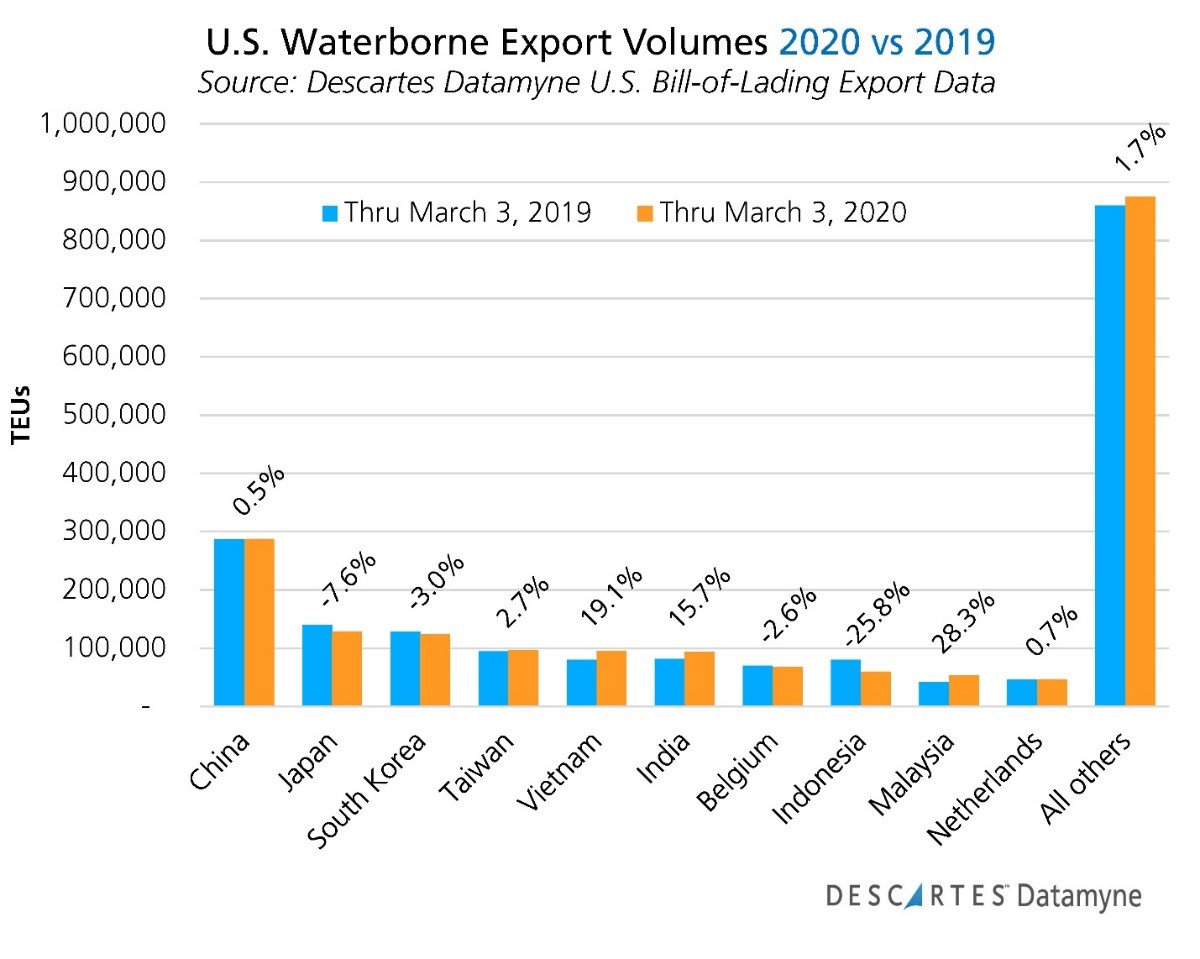

Descartes Datamyne U.S. bill-of-lading import data, updated each day with shipments arriving a day earlier, provides a near-contemporary indicator of the impact of the coronavirus on trade. Keep in mind that this data on waterborne trade does not capture U.S. trade with Canada and Mexico, most of which moves overland.

Here’s is a summary of waterborne import volumes (in 20-foot equivalent units, or TEUs) through March 16:

Compared with 2018 TEU volumes, China’s shipments to the U.S. have dropped more than 20%; inbound cargoes from Hong Kong are down by a quarter. Despite its own troubles with COVID-19, volumes from Vietnam are up 14.8% so far this year.

As market watchers point out (see this FT analysis for instance), it is difficult to tell whether these declines are an accurate measure of the impact of the coronavirus: Shipments might have been bolstered by a build-up of orders ahead of the Lunar New Year – or against the risk that the U.S.-China Phase One agreement might fall apart (announced in mid-December, it was not signed until mid-January).

The BOL export data through March 6 does not indicate a fall-off in demand from China. However, it’s too soon to gauge the impact COVID-19 will have on U.S. production. Indeed, as the coronavirus gains strength as a global pandemic, this data serves best as a benchmark against which to chart the economic ravages of the disease:

COVID-19 Complications: the Price of Oil

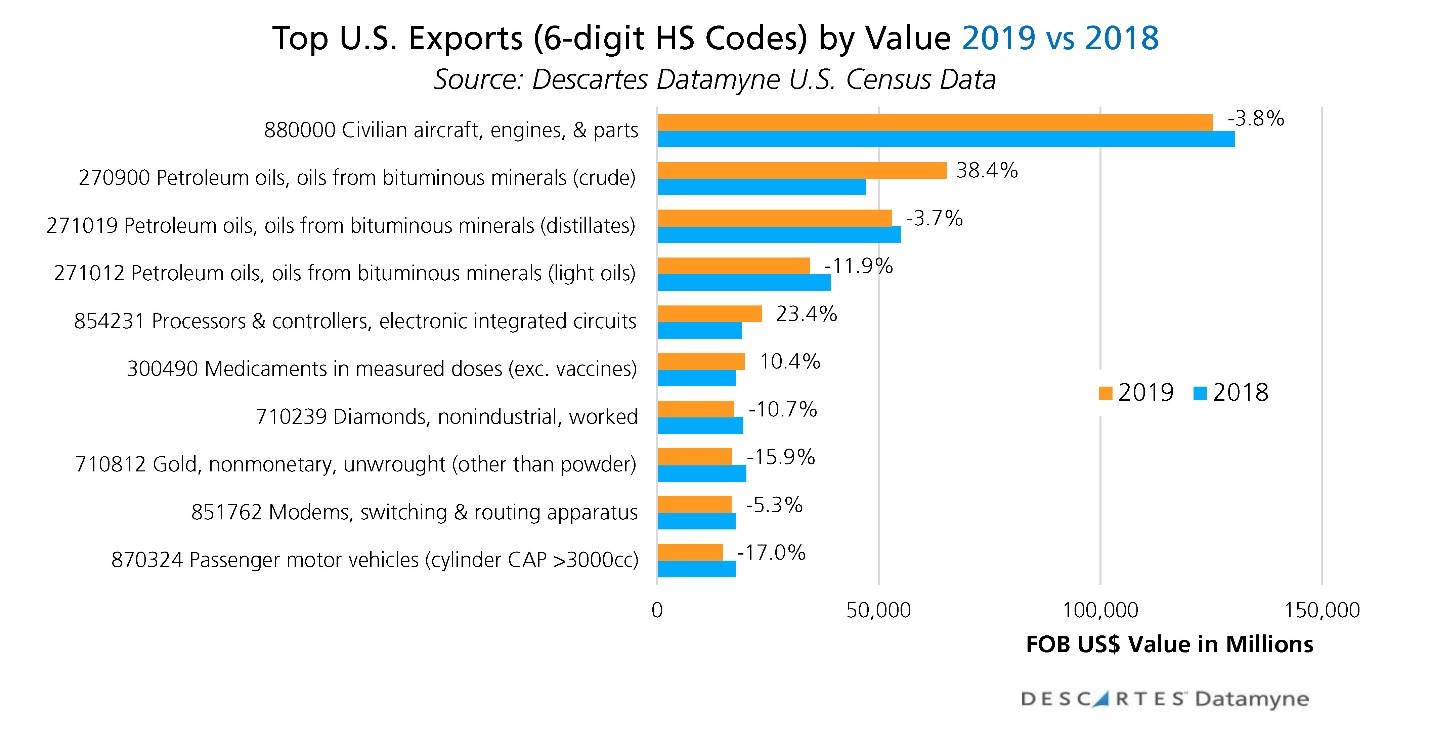

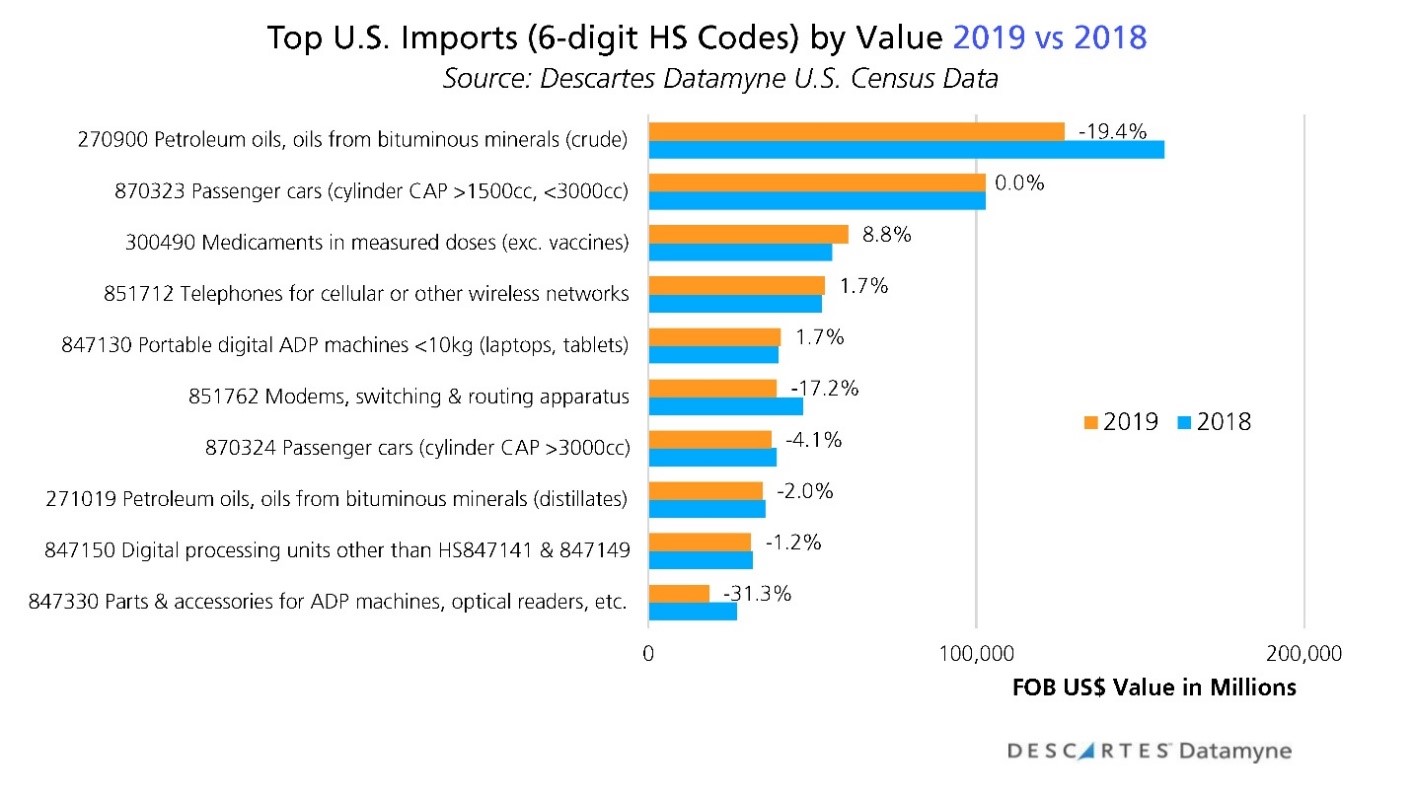

Our Census data on the top products in trade (as denoted by the 6-digit Harmonized System of tariff codes), summarized in the next two graphs, indicates how much the U.S. trade balance hinges on petroleum. In 2019, crude oil exports rose 38.4% as imports declined 19.4%:

Here’s a closer look at the U.S. balance of trade in petroleum from the Census Bureau, showing the shift to exports over imports occurring late in 2019:

As recently as January, the U.S. Energy Information Administration was projecting that the U.S. would become a net energy exporter this year. By mid-February, the EIA was revising its projections of global demand for liquid fuels due to reduced consumption by China because of coronavirus. Modeling its projections on the course followed by the 2003 SARS coronavirus, the EIA was projecting a rebound in Chinese demand by year’s end.

As of mid-March, it’s clear the COVID-19 pandemic will eclipse the SARS outbreak in scale, reach and economic impact.

Further roiling markets, an oil price war has broken out as two of the leading producers of crude, Saudi Arabia and Russia, have abandoned OPEC-led commitments to maintaining the stability of global oil production and, by extension, price. Over-leveraged shale gas and oil producers in the U.S. are especially vulnerable to plummeting oil prices.

COVID-19 and the Cost of Decoupling

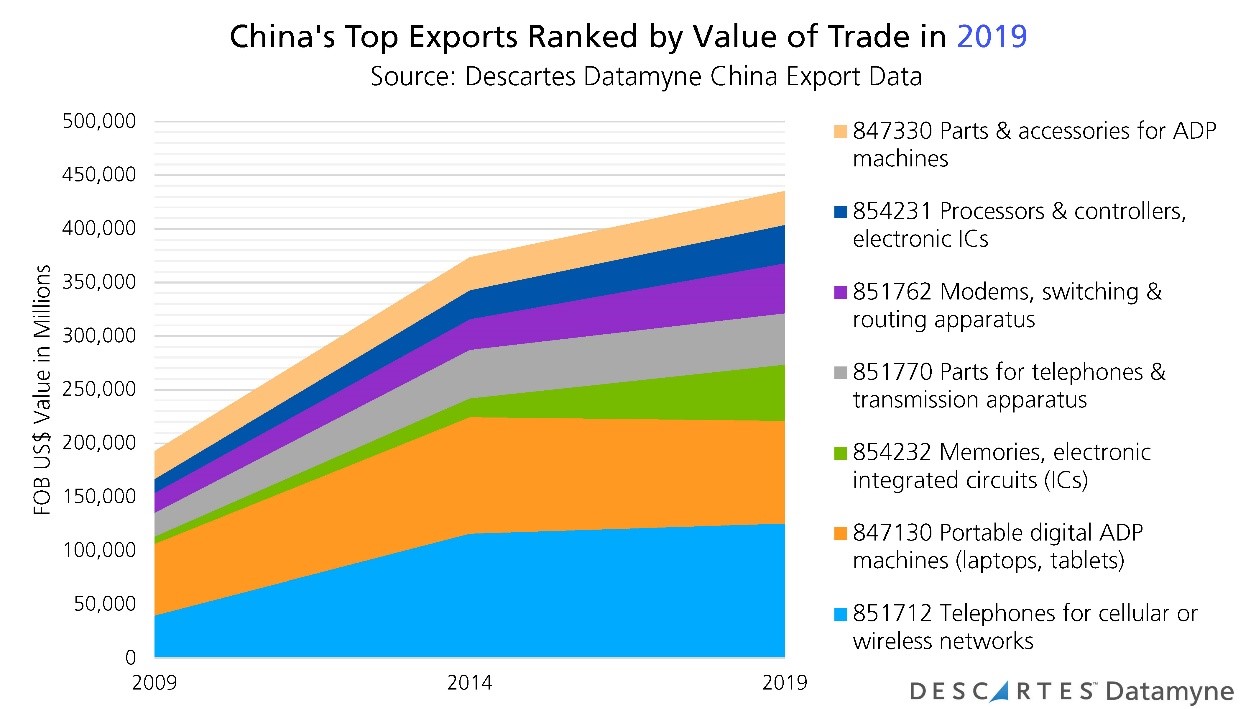

China’s 2001 entry into the World Trade Organization positioned it to become factory to the world. More recently, with lower labor cost countries competing to become global production centers, China launched a new industrial policy aimed at retooling its manufacturing capability to move up the value chain to high-tech products and services.

Our China data provides one measure of the success of the “Made in China 2025” strategy implemented in 2015. As of 2019, China’s top exports were dominated by electronics:

The Economist offers the electronics sector as an example of how intertwined the world’s top trading nations, China and the U.S., have become over the last two decades: Most electronics devices sold in the U.S. are assembled in China. China, in turn, relies on imports for most of what’s needed to make its electronics products – an estimated 55% of inputs used in its robotics, 65% of inputs for cloud computing, and 90% of the inputs used in semiconductors.

The Economist also estimates that it would take 10 to 15 years for China and the U.S. to “decouple” – that is, for China to become self-sufficient in computer chips and for the U.S. to shift to other IT suppliers.

In the wake of rising landed costs for products from China, some companies have unveiled plans to relocate at least some production outside China. Early this February, the coronavirus caused publicly-held companies making smartphones, phone components and modems to issue warnings that first-quarter 2020 earnings goals would likely be missed.

As COVID-19 eclipses 2019’s global market disruptions, it is on course to exact much steeper toll, forcing many industries to recalculate the costs and benefits of diversifying supply chains – and accelerating the process of decoupling the U.S. and Chinese economies.

Related:

Blog:

- U.S.-China Phase One Agreement Focuses on Relationship Reset [Editor’s Note: The coronavirus will almost certainly challenge China to meet its new commitments for U.S. purchasing as part of the U.S.-China trade agreement.]

- Trade Policy Reshapes U.S. Import Peak Shipping

- U.S. Auto Exports and the Impact of Shifting Trade Policy

Resources:

- Our multinational trade data assets can be used to trace global supply chains and our bill-of-lading trade data – with cross-references to company profiles and customs information – can help businesses identify and qualify new sources. Ask us for a free, no obligation demonstration of our data on a product or trade commodity of your choosing – and keep the custom research we create with our compliments.